Understanding Bitcoin

In recent years, Bitcoin has attracted a lot of attention due to its speculative nature, as a safe haven comparable to gold, as an alternative legal tender as in El Salvador, but also due to criticism concerning its power consumption, its potential use for money laundering, and its involvement in criminal activities.

Crypto

Crypto 2023-10-11

2023-10-11

Table of contents

Today, in one way or another, everyone has heard of Bitcoin. Because it's so new, it's sometimes difficult to find an objective, clear definition of what Bitcoin really is. Without going into technical details, this article aims to inform people who know little or nothing about Bitcoin. We will therefore endeavor to explain what Bitcoin is, detailing its origins, how it works, its limitations and its impact on society.

Bitcoin's foundations

1. Origins

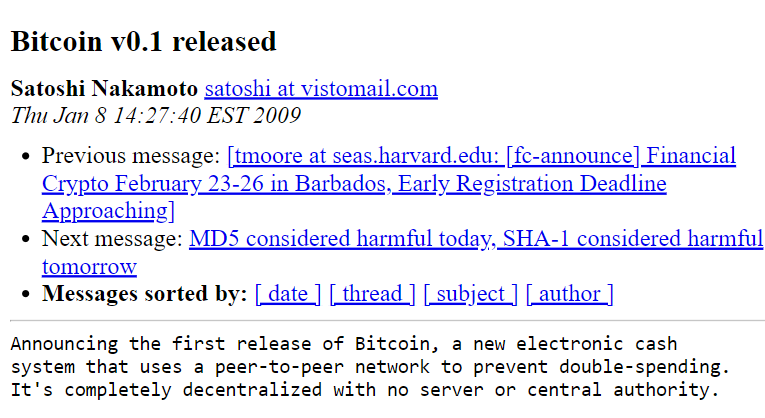

- Bitcoin was created in 2008 by a mysterious figure known as Satoshi Nakamoto. To this day, doubt persists, and we still don't know whether Bitcoin was created by a person, a group of people or an entity. What we do know, however, is that Satoshi Nakamoto mined the first bitcoins for around two years, and to this day holds just over a million of them in various wallets. This enigmatic figure published Bitcoin's source code in 2009 before disappearing in 2011, leaving behind him a disruptive revolution in the making.

2. Bitcoin ou bitcoin ?

- Cryptocurrencies, a term that encompasses cryptographic digital currencies, can serve as both currencies and payment systems, although the two concepts are distinct. Let's take Bitcoin as an example to clarify this often subtle distinction: bitcoin with a lowercase "b" refers to an individual unit of cryptocurrency, while Bitcoin with a capital "B" denotes the peer-to-peer payment system based on blockchain technology. This revolutionary system was introduced in 2008 with the creation of bitcoin, considered the first cryptocurrency ever created. Despite the years since its invention, bitcoin remains the most iconic and widely recognized of all virtual currencies.

3. Decentralization

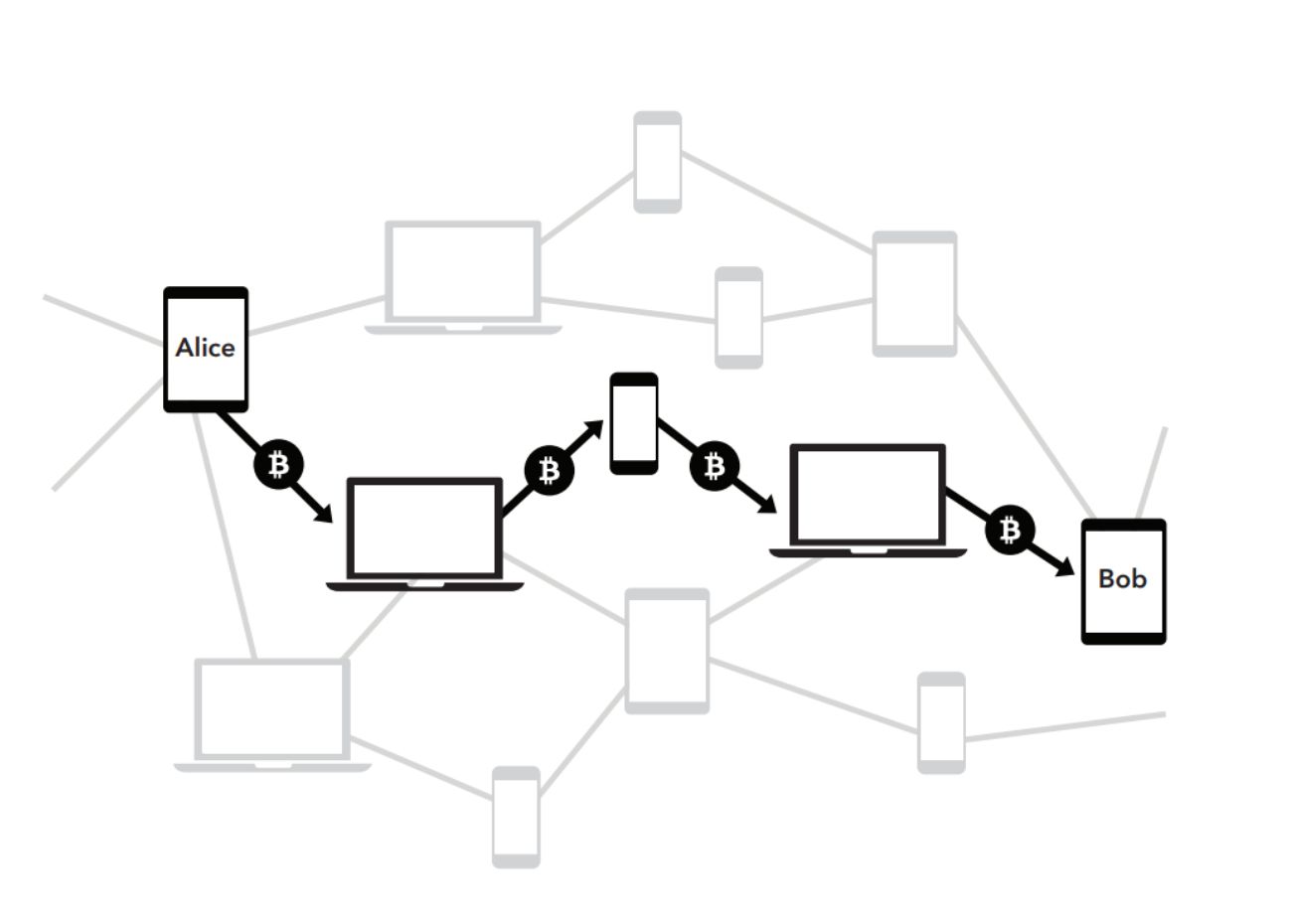

Satoshi Nakamoto's objective is twofold: firstly, to set up a decentralized, peer-to-peer system that enables the exchange of monetary value without the need for intermediaries such as financial institutions. Unlike traditional currencies, bitcoin is not controlled by a central entity, as is the case with the Euro or the Dollar, which are managed by a central bank. The fact that bitcoin is free from a third-party entity makes it unique in its decentralized nature. Bitcoin can therefore exist without the presence of its creator, making it extremely difficult to censor or manipulate. On the other hand, the aim was to introduce blockchain technology and the "Proof of Work" consensus algorithm. For more information on blockchain technology, see our article A complete guide to blockchain technology.

How Bitcoin works

1. "Proof of Work" consensus

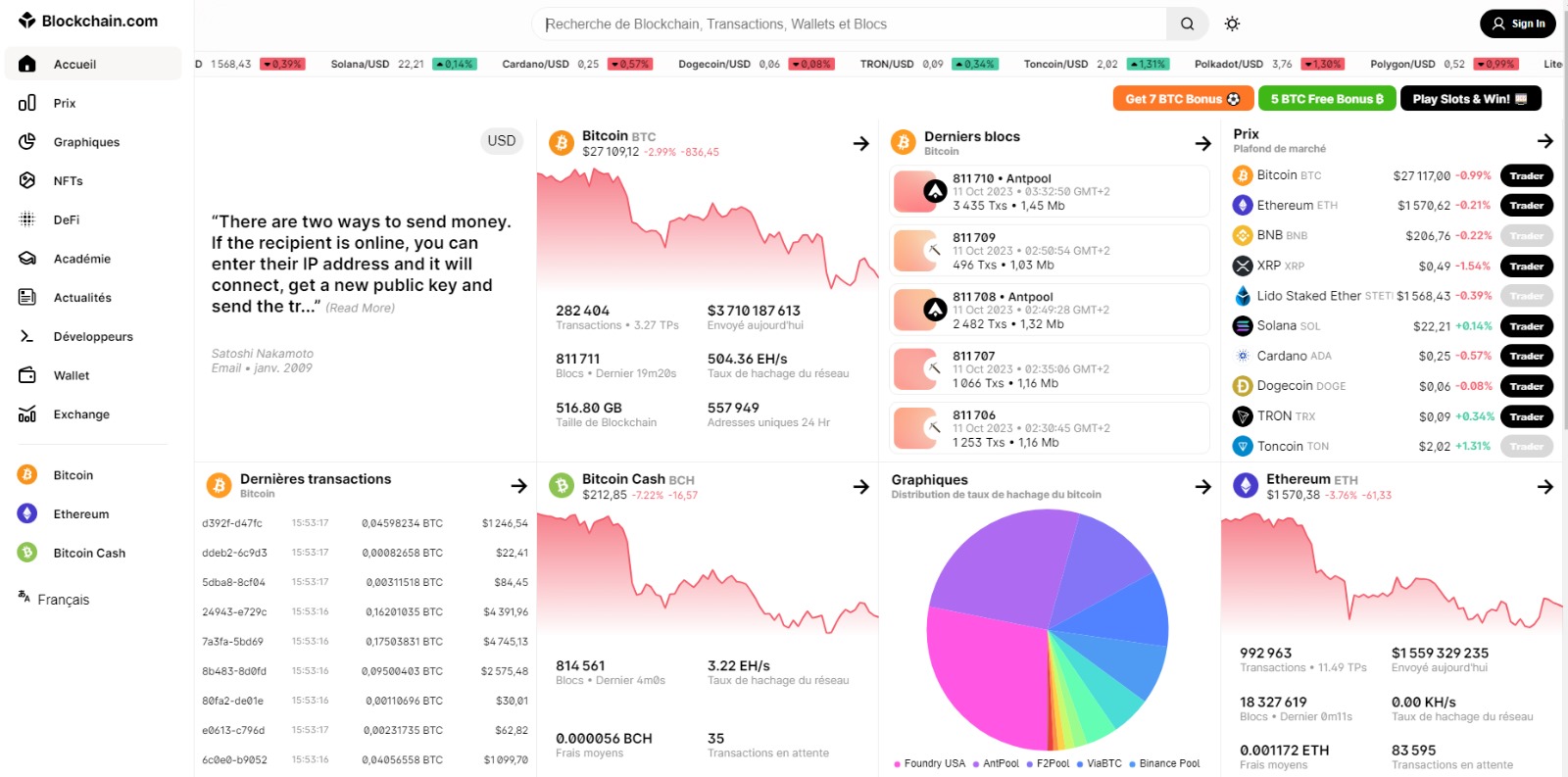

- Proof of Work, introduced by Bitcoin, is a system in which specialized computers, called miners, are tasked with solving complex mathematical problems to validate and secure transactions. When a person sends bitcoins to someone else, this transaction must be verified and added to the blockchain, an immutable public register. Miners solve these mathematical problems by testing different values, thus demonstrating that they have done a great deal of work (proof of work). As a reward for their work, the first miner to solve the problem validates the transaction by adding it to the blockchain, and receives bitcoins in compensation. This process guarantees the security and integrity of the Bitcoin network. Once a transaction is registered on the blockchain, it becomes extremely difficult to modify, which reinforces confidence in the system. This Proof of Work mechanism is fundamental to maintaining the decentralization and reliability of the Bitcoin network, establishing a model of trust for digital transactions.

2. The truth about bitcoin's anonymity

- Contrary to popular belief and media reports, it is essential to understand that bitcoin is not an anonymous currency. On the contrary, the Bitcoin system offers total traceability of transactions, which means that bitcoin is not a tool of choice for illegal activities. Indeed, anyone can track the history of bitcoin transactions by consulting the Bitcoin blockchain using the transaction ID. This transparency is a key element of blockchain technology. However, even if this is possible, thanks in particular to exchange platforms, it remains complex to identify the person behind a transaction. Transactions are carried out using public addresses, which are series of alphanumeric characters. This means that the real identity of the parties involved in a transaction often remains anonymous, unless this information is voluntarily disclosed. Despite the traceability of transactions, bitcoin offers a certain level of anonymity and confidentiality, but it is important to note that this confidentiality is not absolute and depends on the responsible use of the technology by users.

Challenges and opportunities

1. Bitcoin's limits

Bitcoin, despite its revolution in the financial world, has various limitations that need to be considered. Firstly, it is slower and more expensive than many newer cryptocurrencies, making transactions slower and potentially more costly for users. Its price volatility is a source of uncertainty, making its use as a stable currency less reliable compared to other digital currencies. High transaction fees on the Bitcoin blockchain, especially for ordinary users, limit its everyday use and can make microtransactions impractical.

In addition, Bitcoin is primarily suited to simple payments and cannot yet handle large-scale, complex transactions efficiently, which limits its applications in certain sectors. Centralized systems currently offer higher levels of protection and recourse than bitcoin, which may deter some users concerned about their financial security. Despite aspirations to total decentralization, the concentration of miners and wealth in the hands of a minority raises questions about the true level of decentralization of the Bitcoin network. This concentration of power and wealth can potentially compromise the network's security, calling into question the ideal of total decentralization.

Moreover, storing bitcoins on an exchange platform can mean ceding control to third parties, compromising the principle of direct ownership of assets. Cases of hacking of these platforms have been frequent in the history of cryptocurrencies, resulting in the loss of funds for many users.

Finally, although Bitcoin has paved the way for a new financial era based on blockchain technology, it is important to recognize and understand its current limitations for everyday uses. These challenges continue to drive research and development aimed at improving the performance and security of cryptocurrencies overall.

2. A blessing for other cryptocurrencies

- The limitations and challenges faced by bitcoin have paved the way for new opportunities for other cryptocurrency projects. These limitations have highlighted the need for continuous improvements in the field of cryptoassets. Although bitcoin pioneered the world of crypto-currencies, as we have seen above, it is far from perfect. However, these limitations have prompted many developers to innovate and create new cryptocurrencies, each offering solutions to bitcoin's problems. These projects seek to resolve bitcoin's limitations by proposing technologies that are faster, more energy-efficient, more stable, less costly and so on. So these new cryptocurrencies are not just alternatives, but also opportunities for technological evolution. The diversity of these projects contributes to enriching the cryptocurrency landscape, while offering users a wider choice to better adapt to their needs.

3. Alternative currency

Although initially considered an alternative currency, bitcoin is currently legally restricted, being officially recognized as a means of payment only in El Salvador. Outside this country, there is no legislation formally supporting the use of bitcoin as a currency. However, despite this lack of legal recognition in many countries, bitcoin has gained popularity as an alternative currency thanks to its widespread use on exchange platforms. Its popularity also stems from its ability to facilitate fast and relatively inexpensive international transactions. This growing adoption is largely due to the commitment of users and businesses, who see it as a decentralized, globally accessible means of payment, even in the absence of a formal legal framework.

What's more, bitcoin offers a monetary alternative to traditional currencies, enabling individuals, for example, to protect themselves against inflation or government confiscation of their assets. However, it should be noted that the popularity and adoption of bitcoin is not uniform across all countries. Regulations surrounding bitcoin vary considerably across the globe. While the history of this cryptocurrency and its regulatory framework are being written a little more each day, the legal landscape surrounding bitcoin remains complex today.

Lightning network

- The Lightning Network represents an essential scalability solution for bitcoin. Acting as a layer 2 parallel to the Bitcoin blockchain, this off-chain innovation solves the problem of slow transactions and high fees. It enables secure microtransactions between users, processed instantaneously and at almost no cost, while maintaining the system's total decentralization. Transactions take place outside the main blockchain, and are recorded on it once finalized. This technology uses bidirectional payment channels, where users can send and receive payments without requiring each transaction to be registered on the main blockchain. The peer-to-peer aspect of the Lightning Network ensures that two parties can carry out transactions without congesting the main blockchain each time, thus ensuring the speed and security of the Bitcoin network. In short, the Lightning Network offers an effective solution for increasing transaction processing capacity, reducing costs and maintaining security in the Bitcoin ecosystem.

Bitcoin: freedom with responsibility

As we saw in the section on decentralization, bitcoin offers a form of financial freedom, thanks to the absence of intermediaries. However, with this freedom comes responsibility.

1. Financial freedom

Bitcoin is often praised for its potential to offer unprecedented financial freedom. Unlike traditional financial systems, it allows users to carry out transactions without the intermediary of a centralized authority, such as a bank or government. This decentralization gives individuals direct control over their funds, which can be particularly useful in parts of the world where access to banking services is limited.

2. User responsibility

However, with this freedom comes significant responsibility. Bitcoin owners are solely responsible for the security of their funds. Unlike traditional bank accounts, where financial institutions offer some protection in case of fraud or loss of funds, there is no safety net in case of error, hack or loss of funds related to bitcoin use. In other words, users need to take steps to secure their wallets as much as possible by adopting appropriate digital hygiene measures, such as using hardware wallets, backing up private keys in a safe place, using strong passwords, taking measures to protect against theft, and so on.

Bitcoin as a counterweight to the centralized system

- Initially seen as a radical alternative to the centralized financial system, Bitcoin is now seen not as an adversary, but as an essential counterweight to the traditional centralized financial system. Indeed, some believe that the two systems need to complement each other to create a balance. Bitcoin can play a significant role as a counterweight, reducing the risk of drift in a centralized financial system. The blockchain technology underlying Bitcoin offers significant advantages such as transparency, decentralization, democratization of finance and increased accessibility. This innovation not only guarantees the security of transactions, but also ensures a better distribution of financial power, offering the potential for a fairer, more equitable system.

Conclusion

In conclusion, bitcoin, as the pioneer of cryptocurrencies, embodies the essence of decentralization and financial innovation. Thanks to the vision of its creator Satoshi Nakamoto, Bitcoin introduced the revolutionary concept of value transfer without intermediaries, transforming the way we perceive monetary transactions. Lightning Network technology has overcome some of the challenges of scalability and speed, paving the way for instant, low-cost transactions on a global scale.

Although Bitcoin faces limitations, notably in terms of volatility and regulation, its potential to disrupt the traditional financial system is undeniable. By promoting decentralization and financial autonomy, Bitcoin offers individuals greater control over their assets and transactions. What's more, its influence extends beyond borders, offering economic opportunities to the unbanked worldwide.

Bitcoin represents much more than just a cryptocurrency: it embodies a monetary revolution in the making, with the potential to reshape the way we think about and carry out financial exchanges on a global scale.

Sources :

- https://lightning.network/lightning-network-summary.pdf

- E. Bussac, Bitcoin, ether & Cie, ’Guide pratique pour comprendre, anticiper et investir 2019’, Dunod, 2018, Malakoff, pp. 12-16.